Life insurance riders allow you to customize your policy, so you can meet your family’s exact needs.

Life insurance riders allow you to customize your policy, so you can meet your family’s exact needs.

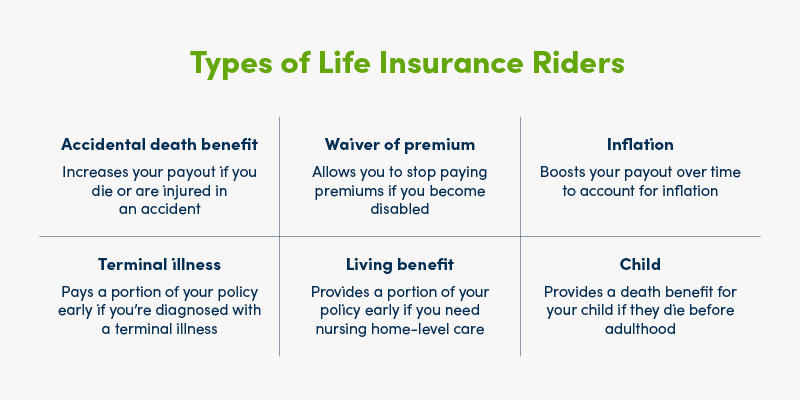

Make your life insurance policy your own by including riders that offer extra financial protection for your child, allow you to stop paying premiums if you are disabled and can’t work, or make other accommodations for your needs.

Some riders let you turn your term life insurance into a permanent life policy or insure an extra person, like your child, without having to go through the whole approval process again.

The waiver of premium rider for disability allows you to stop paying your monthly premiums if you become permanently disabled and can’t work.

With this rider, your insurer will waive all remaining premiums until you are ready to work again, while your coverage remains active. Once your disability ends, your payments start again. If you remain disabled for the length of your term insurance plan, you won’t have to make payments, but your coverage stays in place.

A waiver of premium rider works well for people with a range of financial needs. Whether you run a business or are the main breadwinner in your family, these riders can help protect anyone who would be burdened financially by your lost income. This type of rider can be particularly helpful for high-value policies, which typically come with high premiums that can be tough to maintain after a job loss.

While this benefit can be invaluable, it’s important to review the fine print before signing up. Here are some points to consider:

The terminal illness rider offers a cash payout for you or your loved ones if you are diagnosed with a terminal illness. This rider is often free with your policy or available at a fairly low cost. Also known as an accelerated benefit rider, it’s like a cash advance on your policy. In many cases, you can access a significant portion of your total death benefit, up to 75% in some cases.

These riders are different from critical illness riders, which cover you if you are diagnosed with a serious but curable condition or a chronic illness. Terminal illness insurance is specifically designed to offer your loved ones financial security once you are at the point where recovery is unlikely.

Just like the death benefit from your policy, your family can use this money for whatever they need. It can help defray the costs of your care, cover hospice or medical bills, or replace your income if you are no longer able to work. The funds don’t have to go toward care, though. You can even use the living benefit to pay for a vacation or anything that can help you enjoy your final days with your family and friends.

If you pass away before your term ends, your beneficiary will still receive the remaining portion of your policy’s death benefit. You do not have to repay this money if you outlive your policy.

The living benefit rider provides a payout if you’re diagnosed with a critical or chronic illness or need to move to a nursing home.

On average, nursing home care costs about $7,700 to $8,800 per month in the United States, and about 48% of adults receive some paid senior care over the course of their lifetime. A living benefit rider can give your family peace of mind and a way to cover these substantial costs if you end up needing this type of care. In some cases, the living benefit rider can also help pay for home health services.

Most living benefit riders will pay out benefits if you’ve been diagnosed with a critical illness, chronic illness, or terminal illness. They will need to see proof of your diagnosis before making the payment. In general, life insurance companies often determine that you meet the criteria for this rider when your primary care doctor feels that you are unable to complete two or three of the six activities of daily living: bathing, dressing, eating, toileting, walking, and continence.

If you’re interested in this type of protection, talk to your life insurance agent about any rider options available with your plan. Many companies now include the living benefit rider at no additional cost to you.

If you’re a parent, the child rider provides a death benefit to you if your child passes away before a specific age. This money can provide a financial cushion to cover funeral, medical, or other expenses after a tragic loss. Typically, the payout is a few thousand dollars, and the rider itself is very inexpensive.

Beyond covering immediate needs after a loss, though, many people buy the child rider as a financial investment for their child. A child protection rider is typically term life insurance coverage that lasts until your child is between 22 and 30 years old, depending on the policy. Once your child reaches that age, they can often convert it to a permanent life insurance policy, with coverage up to five times the original amount and without the need for a medical exam. This is a great way to guarantee their insurability and make sure that they are covered once they become adults, even if they encounter health issues before then.

Here are some things to consider when you decide whether to add a rider and which to buy:

There are several things that affect how much you’ll pay for your life insurance riders. Some of these include:

You can find life insurance riders for both term and whole life policies. Keep in mind that each life insurance company offers different options, though. If you have a specific rider you want to add to a new term or permanent life policy, we’ll work to help you find the right provider. We can also help you add riders to your current life insurance plan.